How to Document Damage After a Storm

Extreme weather conditions in Colorado are becoming increasingly common. At the beginning of this summer, who would have guessed that there would be a hail-storm that canceled a Red Rocks concert or a tornado tearing through Highlands Ranch? The property damage resulting from the extreme weather conditions is, unfortunately, becoming more and more common. To set yourself up for success when dealing with your insurance carrier to get proper payments for your loss, it’s important to know the best ways to document these storms and the damage they inflict.

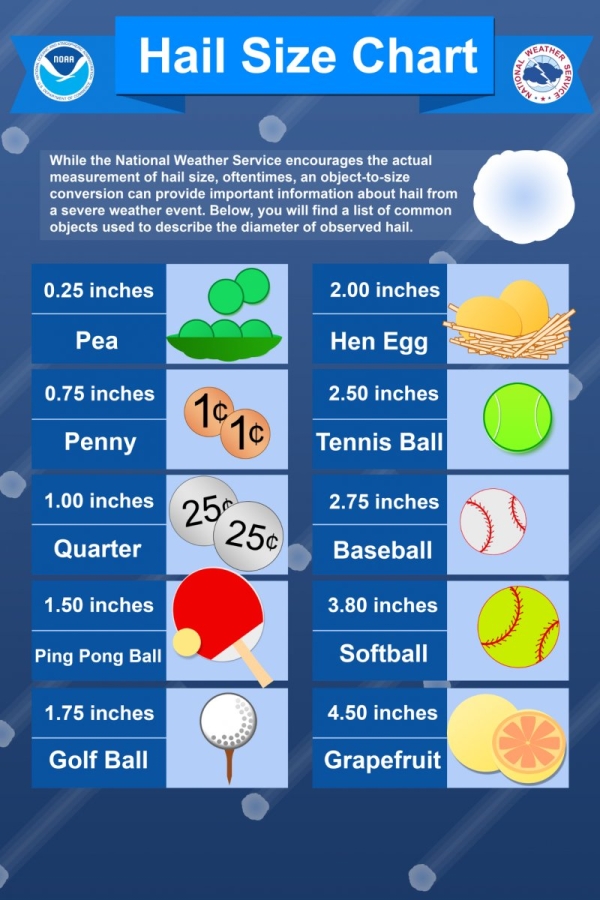

The goal is to document what was damaged and the extent of that damage. Take a hail-storm for example, the gold standard would be having before and after pictures of your roof. Having before and after pictures makes it easier for you to show the damage was a result of the hail-storm and not regular wear and tear. Don’t panic if you don’t have any before pictures, the next best thing you can do is to make a record of the storm and damage. You can do this by taking pictures and videos of the damage; taking pictures of the hail and comparing its size to ordinary household objects; taking videos of the storm; saving weather reports from the day of the storm; etc. For example, if you have a tile roof you might see tiles littering the ground following a severe hail-storm. Take pictures of any broken tiles you find before cleaning up!

These tips apply to any type of damage, whether it be from a hail-storm, wind-storm, flash flood, tornado, or fire. It is important to make a record of the damage and the storm that caused it. You want your record to show:

What was damaged (so take pictures of the roof, windows, siding, floors, etc.),

The extent of the damage (take pictures of anything showing how bad the damage was, for example, take pictures of broken windows, broken branches, etc.),

When the damage occurred (you can save weather reports showing the date of the storm and take pictures with timestamps noting the date of the storm),

Any steps you took to prevent the damage or prevent any further damage (for example, take pictures of tarps on your roof to prevent leaks).

Once you file your claim, it’s important to make a record of any communications you have with your insurance carrier. Document when and how you notified your carrier of the damage and any conversations you have -- don’t be afraid to follow up via email to confirm important conversations.

Be sure to save any and all documentation for a few years, just in case anything comes up in the future. Sometimes, after you have the repair work done on your roof that your insurance carrier approved, you may have more leaks in the future, because it turns out that there was more damage than what your carrier anticipated.

Remember, even though making a record is important, nothing is more important than your safety!